Personal Budgeting Checklist: Your Must-Have Plan for Effortless Finance

Managing your finances effectively can often feel overwhelming, but with a personal budgeting checklist, you can create a clear, manageable plan that steers you toward financial success. A well-structured personal budgeting plan isn’t just about tracking expenses—it’s about setting priorities, making informed decisions, and ultimately gaining control over your money without stress. Whether you’re starting from scratch or looking to refine your budget, this guide will walk you through the essentials to build a personal budgeting checklist tailored for effortless finance management.

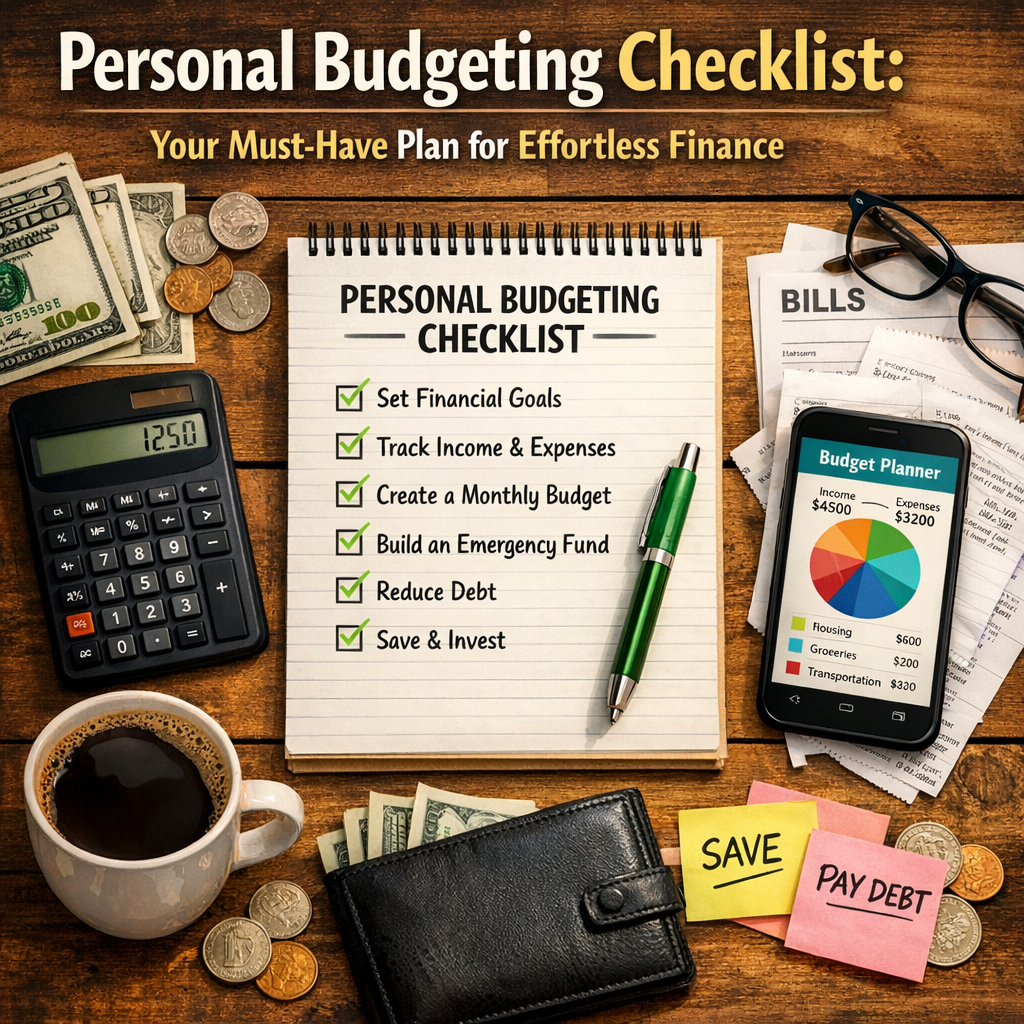

Why You Need a Personal Budgeting Checklist

A budgeting checklist serves as a roadmap for your financial journey. It breaks down the complex world of income, expenses, savings, and investments into actionable steps. Without a plan, it’s easy to lose track of where your money goes or fall into unhealthy spending habits. Adopting a personal budgeting plan helps you:

– Avoid overspending and reduce debt

– Allocate funds for important goals (like emergencies or retirement)

– Increase savings and improve your credit score

– Make mindful spending choices that align with your values

With your priorities and financial health clearly outlined, you can avoid surprises and grow your wealth steadily.

Step 1: Assess Your Financial Situation

The first step in your personal budgeting checklist is understanding exactly where you stand financially. This means gathering all relevant financial information, including:

– Your total monthly income (after taxes) from all sources

– Fixed expenses like rent/mortgage, utilities, insurance, and loan payments

– Variable expenses such as groceries, dining out, entertainment, and transportation

– Outstanding debts, including credit cards and personal loans

– Current savings, investments, and any other assets

By compiling this data, you establish a baseline for creating your budget and identifying areas for improvement.

Step 2: Define Your Financial Goals

No personal budgeting plan is complete without clear goals. Do you want to build an emergency fund, save for a vacation, pay off debt faster, or plan for retirement? Setting specific, measurable objectives helps you stay motivated and track progress. Categorize your goals into short-term (next 6-12 months), medium-term (1-5 years), and long-term (5+ years) so your budget reflects your priorities.

Step 3: Create Categories for Your Budget

A detailed budgeting checklist involves organizing your expenses into clear categories. Typical categories include:

– Housing (rent/mortgage, utilities, maintenance)

– Transportation (car payments, fuel, public transit)

– Food (groceries, dining out)

– Insurance (health, auto, home)

– Debt Repayment (credit cards, loans)

– Entertainment/Recreation

– Savings and Investments

– Miscellaneous

By grouping expenses, you can easily identify which categories consume the most resources and where you can make adjustments.

Step 4: Track Your Spending Regularly

Consistency is key when following a personal budgeting plan. Track every expense diligently, either with a budgeting app, spreadsheet, or a simple notebook. Regular tracking helps you:

– Recognize spending patterns

– Spot unnecessary expenditures

– Adjust your plan proactively before overspending occurs

Make it a habit to review your spending weekly or monthly to keep your budget aligned with reality.

Step 5: Plan for Emergencies and Savings

An often-overlooked part of any personal budgeting checklist is setting money aside for emergencies. Aim to build an emergency fund that can cover 3-6 months of living expenses. This fund provides a financial cushion during unforeseen circumstances like medical bills or job loss.

Additionally, automate savings contributions to retirement accounts or investment plans. “Pay yourself first” is a powerful strategy that ensures saving becomes a priority in your financial plan rather than an afterthought.

Step 6: Review and Adjust Your Budget Monthly

Life changes, and so should your budget. Review your personal budgeting plan at least once a month. Look out for:

– Changes in income (raises, new job, side gigs)

– Adjustments in expenses (bills, subscriptions, lifestyle changes)

– Progress toward your financial goals

Adjust your spending limits or savings targets accordingly to keep your budget realistic and effective.

Step 7: Stay Committed and Seek Support

The best personal budgeting checklist is only as good as your commitment to it. Stay motivated by celebrating small wins along the way, such as paying off a credit card or hitting a savings milestone. Don’t hesitate to seek external support if needed—financial advisors, online communities, or budgeting workshops can offer valuable guidance and encouragement.

—

Final Thoughts

A personal budgeting checklist simplifies the complex task of managing money and turns it into a structured, stress-free process. By evaluating your finances, setting clear goals, categorizing expenses, tracking spending, saving smartly, and reviewing regularly, you can create a powerful personal budgeting plan that works for your unique lifestyle.

Start today—your financial freedom is just a checklist away.